Banking, Bastards and the Trolley Dilemma

The Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry is likely of little surprise to most people. “All banks are bastards” is a generalisation often endorsed by the community as a way of illustrating financial robustness, that most have suspected, or known, for a long time, and the Royal Commission confirms the obvious.

Yet, likely no one sets out to do wrong. It is far more complicated than that.

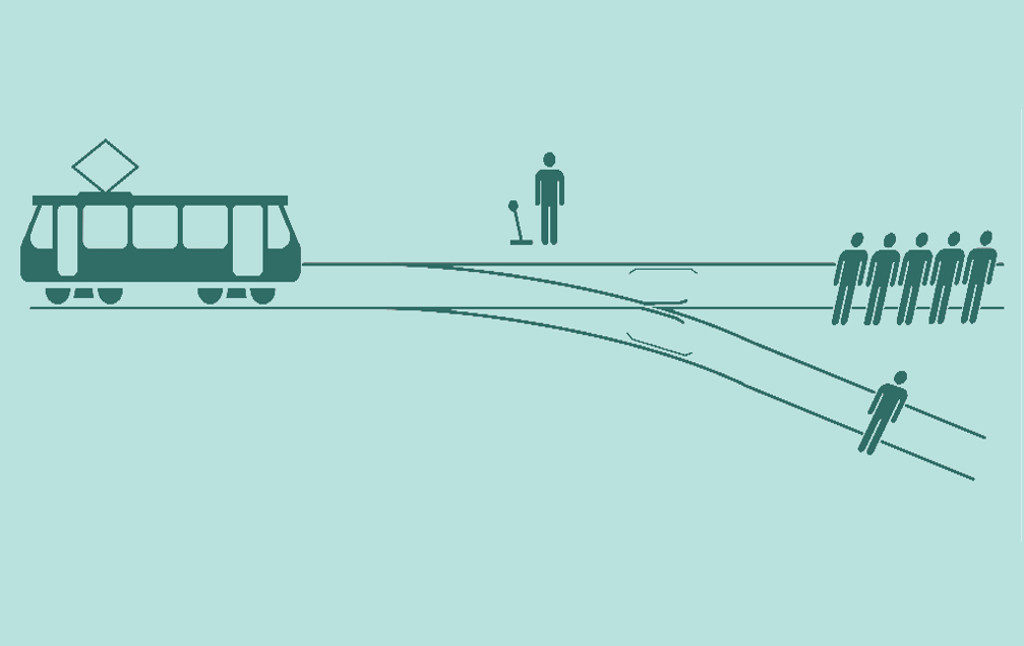

The Trolley Dilemma is an experiment used to illustrate the challenges in making ethical decisions. What may be the right way for one person, may be viewed as wrong to another. A summary of the Trolley Dilemma follows.

- You are driving a run-a-way tram

- The brakes are not working and there is no way to stop it!

- Straight ahead there are five people who will die if you go forward

- Or, you can switch tracks, one person would be hit and die

- Would you go forward and kill 5 or switch tracks and kill 1? Why?

- What if the one person was a loved one or leading thinker / artist?

- What if the five were bad people, e.g. the KKK or known murders?

- You are no longer driving the tram, but on a bridge, where there is a fat man looking over. If you pushed him, he would fall in front of the tram, stop it, die, but save the other six people. What would you do?

- What if the man on the bridge was an evil, known villain?

- What would you do?

You can read more on the Trolley Dilemma here, or by watching the fascinating series of ethical justice videos ‘What’s the Right Thing to Do?’ by Harvard’s Michael Sandel. (The Trolley Dilemma is widely used when considering situations such as what driverless cars should do.)

In a corporate setting the Trolley Dilemma could be translated to decision makers. Typically the answer comes back to ‘what is best for the company (or even individual)?’ Maximise profit, the basic premise of business throughout time, while potentially sacrificing groups of customers, staff and/or other stakeholders. It is rarely win-win in business.

“The gap, as I see it, is that NAB does aspire to do the right thing by every customer every time and everywhere and we’re a long way from that. We’ve got an absolute mountain to climb in NAB in order to achieve our aspiration for the bank.”

Outgoing NAB Chairman Dr Ken Henry

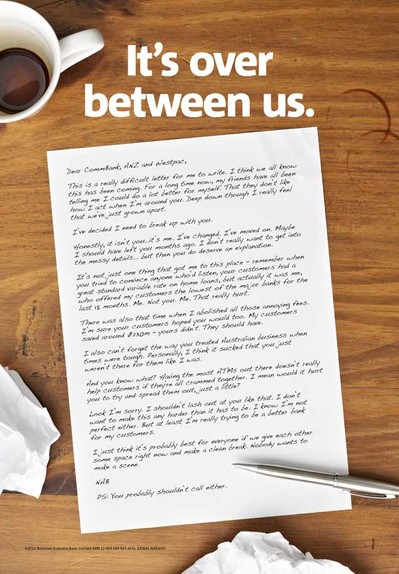

This from one of Australia’s four BIG banks, who’s advertising spin has tried hard to tell a far more customer focused business story than reality.

It is important to stress that the Royal Commissioning isn’t about bad NAB, it is about entrenched misconduct across the banking, financial services and superannuation sectors, and concerning levels of placing profit and individual gain above service to customers.

“In almost every case, the conduct in issue was driven not only by the relevant entity’s pursuit of profit but also by individuals’ pursuit of gain, whether in the form of remuneration for the individual or profit for the individual’s business. Providing a service to customers was relegated to second place. Sales became all important. Those who dealt with customers became sellers. And the confusion of roles extended well beyond front line service staff. Advisers became sellers and sellers became advisers.”

Page 1-2 of the Final Report of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, Volume 1

It is tricky, as our community by and large endorses such bad behaviour of banks and other financial institutions. From our research for financial institutions, people actually expect a bit of mongrel in our banks, this is how they protect the money of customers. This is one of the challenges smaller alternatives such as credit unions and other ‘not for profits’ have. Campaigns promoting that they are nicer than banks generally fail, as people are typically seeking better deals from those offering more security, generally viewed as the major banks. And, sadly the ‘nice guys’ are actually not viewed any nicer in reality than the big banks, as they use the same models and similar teams to attract and retain customers.

Irrespective of the Royal Commission, the BIG banks continue to be a safe bet on the stock exchange. Looking at today’s Australian Securities Exchange, the banks continue to be amongst the strong investments on the Australian Stock Exchange (In today’s newspaper three of the four are listed the top 10 of ‘People’s Choice’ and Westpac just outside of this) – NAB, ANZ, CBA and Westpac. A likely relief to the boards, investors and staff of banks and other financial institutions – “well played team.”

It is important to note that the banks are by no means the only bastards. The Royal Commission into Aged Care Quality and Safety is currently in progress and likely to report much inappropriate behaviour. Our politicians are often accused of eroding trust through suspect antics, and other leaders of large and smaller enterprises find themselves making unpopular decisions. It is hard being a leader. Having an ability to make hard, unpopular and even ethically questionable decisions can be important.

Politicians need to play politics to achieve outcomes. One segment of the community may gain (e.g. those in a targeted electorate), yet others may be sacrificed and disadvantaged. To get small wins in the long term, may require questionable sacrifice. A good politician needs to play the game.

Boards are typically focused on solvency, ever growing profit (often unrealistically), a rising share price and meeting legal obligations. Customers, even with the rhetoric, are too often a mere means to an end, a secondary or even tertiary consideration. From our research, customers are typically lazy when unhappy, and rarely or are slow to switch away from poor service, as the risk and hassle of shifting is not deemed worth it.

“It is better the devil you know.”

Importantly, studies illustrate that our bankers are more trusted than other professions such as politicians, real estate agents and advertising people. (More: UK US Australia). While we are observing declining levels of trust in our leaders, to an extent such lack of perceived honesty is largely allowed by our community.

Royal Commissions and other questionable behaviour is likely less about legalities than ethics. Laws set objective boundaries, ethics are often subjective and one person’s right is another’s wrong. As individuals we may view ourselves as holding high levels of ethical values and care for others, yet with challenging moral dilemmas our choices may be questioned.

For our disgraced bankers, it is likely they had escalating growth targets set by the Board on profit, share price, bonuses and other measures that were not possible from simply delivering on customer needs and expectations. Difficult, and sometimes unethical decisions needed to be made. In challenging environments, and entrenched cultures, even with the rhetoric, it isn’t possible to make the customer priority #1.

It is also fair to assume that our small to medium businesses will also be placed in situations where difficult and unpopular or questionably ethical decisions need to be made. A start-up launched as a social enterprise needing to pay bills, wages et cetera, finding it more difficult to generate sufficient revenue and/or manage costs. A business attracting investors, which increases profit and growth targets, leading to the need to compromise on the founding ethos and values – “at least in the short-term.”

Most people do not set out to be bad. People generally intend to do good, but when faced with dilemmas they need to make complex and often quick decisions, with conflicting outcomes. Not everyone wins, and often the decisions that need to be made by corporate and government leaders, and even ourselves, are not simple and counter to how others in a similar situation may have hypothetically responded.

So, how do we deal with making more ethical decisions moving forward? This is far more complex than switching from ‘BAD’ to ‘GOOD’ as people are almost always fundamentally good, they just make unpopular and/or wrong decision at times. Businesses focusing on perpetual growth in profitability, the share price and bonuses linked to sales can move the focus of such organisational cultures away from customers and the community.

Like the Trolley Dilemma, leaders make decisions that advantage and disadvantage some customers, staff and stakeholders over others, and at times they sacrifice groups of individuals by pushing them off the non-literal bridge just like the ‘fat man’ innocently minding his own business.

It comes back to placing the role of ethics towards customers, staff and other stakeholders at the forefront of decision making along with financial and other key metrics. Embedding solid principles of ethical decision making, beyond legal obligation, across organisational cultures, in boards and c-suites.

Hopefully one of the key outcome of the Banking and Aged Care Royal Commissions is that customers and the wider community are more aware that there are rights and standards of ethics to expect, and if their current providers are behaving badly, more empathetic, responsible and truely customer focused competitors are ready and waiting to offer a better product or service, with more ethical values based cultures and guidelines.

Please be truly customer and human centric. It is ethically right. 🙂